Foreword: While the world’s focus has recently been on the football World Cup, it is worth mentioning another large contributor to the Brazilian economy – iron ore. Brazil remains the second largest seaborne supplier of iron ore to China (behind Australia) and is home to the world’s largest iron ore producer, Vale. Following a recent research trip, I believe Brazil remains crucial to the supplydemand balance in the seaborne iron ore market and will have significant ramifications for prices over the medium to long term.

Brazil is a large, high-quality iron ore supplier

Morgan Stanley estimates that Brazil will export 320 million tonnes (mt) of iron ore in 2014, of which Vale will export 265mt. What is often not mentioned when comparing Brazil to Australia, is the superior quality of Brazil’s iron ore. Average iron ore grades from Brazil are well above the benchmark 62% iron (Fe) content that is often quoted. Vale produces products with up to 66% iron ore content. This is in stark contrast to Australian iron producer, Fortescue Metals, which produces sub-60% iron ore content. The key saleable iron ore grade from Rio Tinto, who produces Australia’s highest quality iron ore, is 61% (for Pilbara Blend Fines).

A shift to a supply surplus has implications for pricing

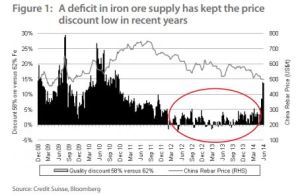

In recent years, a deficit in the supply of iron ore meant the grade differential between the various iron ore qualities did not result in any significant discounting. The adjustment to the lower iron content was made to the benchmark pricing plus an additional small penalty for the Chinese mills taking lower grade than they would otherwise like for their sinter feed (iron ore feed to the blast furnace). For the producers of low-grade products this was an excellent outcome but unsustainable.

Looking back over a longer time horizon, this has not been the case. When the market moves from a deficit of iron ore supply to a surplus, the steel mills are less willing to take a lower-quality product. The lower-quality product produces more slag in steel making (and a less efficient blast furnace), requires steel mills to find higher-quality iron ore to blend and increases handling costs of iron ore as low-quality ore must be blended with a high-quality product. As a result, the small penalty that is separate from the grade adjustment has in fact been a significant penalty in the past, as high as 30% in 2009 (as highlighted in figure 1).

We are now moving into a phase where the supply of iron ore has caught up with demand for iron ore. In 2014, new seaborne supply in the iron ore market will be approximately 110mt per annum. For the first time since 2008, Chinese domestic iron ore supply to steel mills will fall materially (by over 70mt). 2015 will see close to a further 100mt from both Brazil and Australia. The additional tonnes in 2014 are expected to be high-grade iron ore (60% to 66% Fe) from Rio Tinto (+50mt), Vale (+40mt) and other Brazilian producers (+20mt).

Steel consumption will increase by approximately 3% in 2004 from 2013 levels. Over the same period, seaborne iron ore supply will grow by 16%. The large increase in supply relative to the steel consumption increase will be balanced by the closure of high-cost production both domestically in China, but also from other non-traditional producers such as Africa and the Middle East. We believe this should provide a floor in the iron ore price of around USD 90 to 100 per tonne in 2014.

Quality not just quantity

The reason this will be a golden age for Brazilian iron ore is due to its quality. Vale produces high-quality iron ore, particularly in the northern system (region), with Vale’s Carajas project being among the best quality, large scale iron ore mines in the world. In addition, the new expansion project at Carajas, S11D, is expected to add 90mt per annum of supply by 2016. The cost of producing the S11D iron ore is a mere USD 11 per tonne (excluding freight costs), reflecting the size of the iron ore body, quality of the deposits and lower labour costs.

Compare this to Rio Tinto, which is in the mid-USD 30s per tonne (excluding freight costs) and the superior economics of the new Vale iron ore are easy to see. Adding another USD 20 per tonne for freight to China and Vale will deliver iron ore to Tianjin port for approximately USD 30 per tonne, while also receiving a premium to the 62% Fe index which will make the margin for the Vale product at almost USD 60 per tonne.

It is not just the Vale iron ore that has such great economics. A review of other iron ore producers in Brazil shows that the cost delivered to the port in Brazil for many producers is in the low USD 20s per tonne. The lack of infrastructure to load ships is preventing this production reaching the seaborne market. Port owners are able to command over USD 20 per tonne to load a ship. Add another USD 20 per tonne for freight to China and these producers are delivering iron ore to Tianjin at USD 60 per tonne. This cost is still well below the likes of Fortescue Metals and well below some of the higher-cost mid-cap Australian producers – but above Rio Tinto and BHP.

What has held back Brazilian supply?

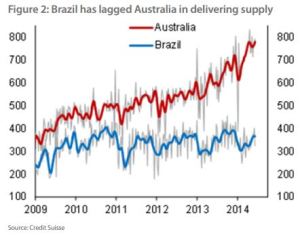

The question then becomes, if the economics are superior for these Brazilian projects, why have they failed to deliver net new tonnes to the seaborne market (as evidenced by figure 2)? The difficulty in delivering infrastructure solutions can never be underestimated. The junior Australian iron ore miners (those who produce less than 30 million tonnes of iron ore per year) who do not own rail or port facilities understand this challenge. This lack of infrastructure has hampered their ability to deliver tonnes to the market when prices were more favourable. Brazil suffers a similar fate. For the junior miners in Brazil, the biggest infrastructure problem they face is port access. Currently, two key companies control the major export ports for iron ore. They are Vale and Trafigura.

Vale has an incentive to keep iron ore prices supported and fill the market with their own tonnes of iron ore. They benefit from the port fees they are charging to load ships and also benefit from the slightly higher iron ore price. If they increase the port capacity, Vale will likely lower the loading fee of approximately USD 20 per tonne and will increase seaborne supply, helping to push the iron ore price lower.

Trafigura is a global trading house. By controlling supply, they can ultimately influence pricing which they rely on for their trading business. Therefore, there is not a great incentive for port expansion for non-Vale tonnes. It is this tonnage that is uncertain to come to the market by 2016 as forecast.

In addition to infrastructure challenges in Brazil, the other issue Vale has faced is environmental approvals. Carajas sits in the mountains of Northern Brazil. Deep in the jungle, the environmental challenges of developing mining operations has forced the government to consider the impact on the natural environment. Among the challenges are the potential destruction of caves and forest areas which affect flora and fauna. Until recently, this has been the biggest hurdle in the expansion of the S11D project.

The tide is turning for Brazil iron ore

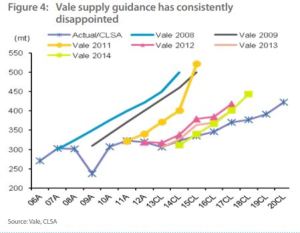

It appears that the government is finally turning to a more favourable view on Vale expansion projects. In July 2013, the Brazilian government approved the construction of S11D, three years after the company originally expected to be granted approval. There remains one licensing hurdle to completion and the exporting of ore, and that can only be achieved once construction is complete. The recent approval shows the intent of the government to allow Vale to grow and suggests the years of frustration that have delayed production expansion (as evidenced in figure 4) may finally be over. With these tonnes, it will further reduce the need for low-quality iron ore, which suggests the low-grade iron ore produced by the Australian mid-tier miners (including Fortescue) could struggle to find a home.

Increased focus on the low-grade iron ore discount

Vale has spoken of their desire to push the low-grade discount down further. They are opening a blending facility in Malaysia, with the purpose of blending their high-grade, low impurity Carajas ore with their lower-quality, higher impurity southern system ore. The result is a product of around 64-65% iron content. The CFO of Vale recently confirmed to me during a meeting while on the research trip to Brazil, their goal is to address the company’s concern that they were not receiving a big enough premium for their high-quality iron ore (the flip side being that Fortescue was not receiving a big enough discount for their low-grade iron ore). Vale has not been happy with Chinese steel mills blending their product with lower-grade product – from Australia in particular.

It will be interesting to follow the grade discount rather than the headline price over the next six months. The big producers such as Rio Tinto, BHP Billiton and Vale have the ability to increase high-grade iron ore production and shift the mix to meet market demands and take advantage of premiums or avoid discounts. Fortescue on the other hand (and the junior iron ore miners) are more limited. It should be noted that the junior miners in a lot of cases have developed resources that BHP Billiton and Rio Tinto no longer wanted when the iron ore price was in the USD 30s per tonne. The junior minors have limited flexibility to improve grades without increasing production costs substantially.

The situation developing in Brazil will be making many Australian iron ore miners sit up and watch. Brazil remains the key unknown to where prices and discounts in the iron ore market will sit. Delivery of net new tonnes will be the key for consensus pricing to sit around USD 85 per tonne. Failure for Brazil to deliver net new tonnes in 2016 will see the longterm price rise above the market consensus. This would be a positive for the lower-grade producers including Fortescue and Atlas.

In the short term however, the market will remain well supplied for the remainder of this year as Chinese steel consumption seasonally weakens in the third and fourth quarters. The cost curve has shifted down structurally. USD 100 per tonne will now be the new USD 120-130 per tonne. Grade discounts are now the focus, rather than the headline benchmark price. The potential risk, particularly for low-grade iron ore producers, is how large these discounts can grow.